Federal student loan interest rates for the 2023-24 academic year are live, and they are the highest they’ve been in at least a decade. Interest rates for undergraduate direct subsidized loans, for example, haven't been this high since hitting 5.6% for the 2009-10 school year.

The new rates apply to all loans taken out from July 1, 2023, to June 30, 2024, according to the Education Department. The interest rate for an undergraduate direct loan is 5.5%. Graduate students taking out direct loans will face a 7.05% interest rate. PLUS loans for graduate students and parents come with an 8.05% interest rate. Here’s how the new student loan interest rates compare with the 2022-23 academic year:

- Direct subsidized and unsubsidized loans for undergraduate students: 5.5% for the 2023-24 academic year; up from 4.99% for the 2022-23 academic year.

- Direct unsubsidized loans for graduate students: 7.05% for the 2023-24 academic year; up from 6.54% for the 2022-23 academic year.

- PLUS loans for graduate students and parents: 8.05% for the 2023-24 academic year; up from 7.54% for the 2022-23 academic year.

“For students and families considering new federal loans, it's crucial to carefully evaluate the implications of these rate changes,” the National Foundation for Credit Counseling, a nonprofit consumer advocate agency, said in a statement.

Though federal student loans are getting more expensive, they’re still usually a better deal than private alternatives.

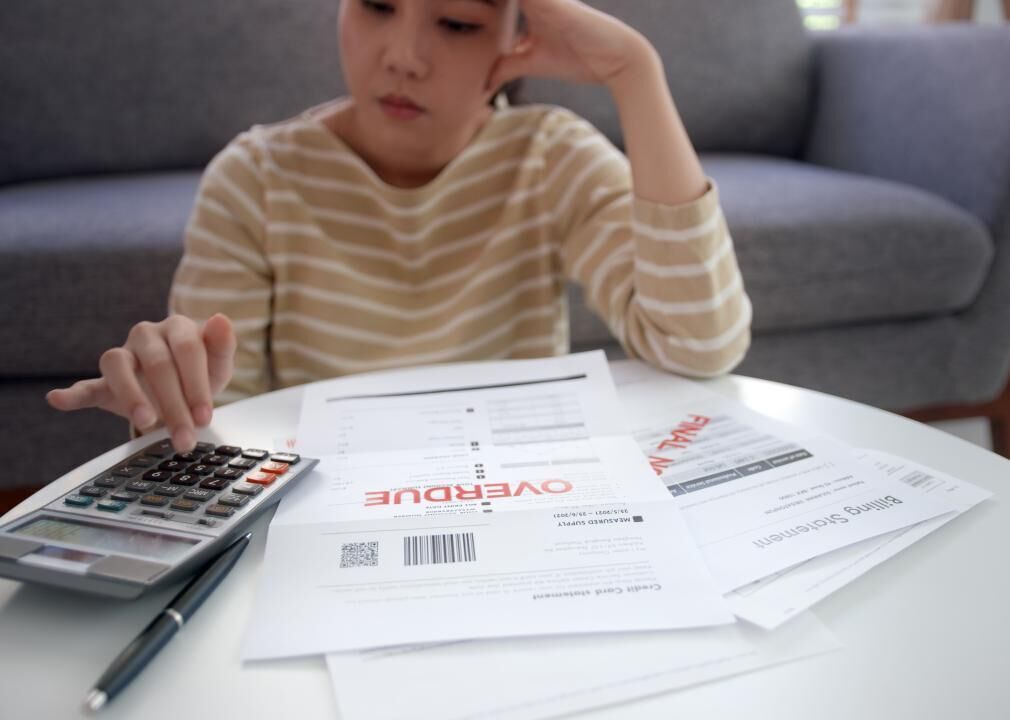

What higher interest rates mean for incoming and current students

As interest rates rise, you pay back more on the amount you borrow.

For example, a $5,000 unsubsidized federal direct undergraduate loan on a standard 10-year repayment term would cost you $1,361 in total interest at the 2022-23 interest rate of 4.99%. If you borrow the same amount for the 2023-24 school year at the new 5.5% rate, assuming the same repayment term, you’ll pay an additional $150 in interest.

Keep in mind that the new federal interest rates apply to federal student loans taken out for the 2023-24 academic year only. Existing federal loans aren't impacted by the new rates.

The federal student loan interest rate bump comes as the cost of borrowing increases for consumers across the board, in areas like car loans, mortgages and even private student loans.

Fixed rates on private student loans have generally trended upward over the past year, according to an April 2023 NerdWallet analysis. If you’re supplementing financial aid with private student loans, you’ll likely feel the impact of higher interest rates a little more.

Comparing federal and private student loan interest rates

Though federal student loans are getting more expensive, they’re still usually a better deal than private alternatives, and borrowers should use federal loans before they consider private loans. Fixed interest rates advertised by private lenders range from 5.99% to 13.78%, and variable interest rates are around 5.61% to 13.27%, based on a May 2023 NerdWallet analysis.

Federal student loans have a fixed interest rate that is set by Congress annually. Interest rates for private student loans can be fixed — locked in for the life of the loan — or variable.

Also, the rate offered by private lenders can vary based on income, credit score and other factors used to determine a borrower’s ability to repay. Federal student loan interest rates don’t depend on those factors. All eligible borrowers will receive the same predetermined rate.

But in addition to comparing interest rates, there are also other factors to consider.

Federal loans come with benefits that protect borrowers, like repayment programs based on income and loan forgiveness for those who qualify. Private loans lack these options.

It can also be harder to qualify for favorable loan terms with a private lender. You’ll typically need a credit score of 600 or higher, or a co-signer with strong credit, to get the lowest advertised rates. Most federal student loans don’t require a credit check or co-signer.

How to minimize student loan costs

Even when interest rates are high, there are still ways to minimize the amount that you borrow.

Submit the FAFSA. The Free Application for Federal Student Aid is your ticket to federal financial aid — including money you don’t have to pay back, like grants, scholarships and work-study programs.

Prioritize “free money.” Outside of federal aid, you can apply for scholarships and grants through nonprofit organizations or with your school directly. These alternative funding options can alleviate the burden of student loans, advised the NFCC.

Max out federal student loans before borrowing from private lenders. Federal loans will likely be the most affordable route, and you’ll have access to income-driven repayment programs and other protections to make paying your student loan bills more manageable

Factor in future earnings. Investing in education can be a wise long-term decision. But it's essential to compare the cost to potential future earnings, according to the NFCC. One rule of thumb is to avoid borrowing more than your expected starting salary once you graduate.

Consider making in-school payments on your loans. Payments on federal loans and many private loans can be deferred while you’re in school. So you don’t have to pay while in school, but you can.

If you have a federal unsubsidized loan, interest will accrue while you’re in school. Making payments while in school will decrease the amount of interest that’s added to your loan once you begin repayment. In-school payments to subsidized loans will go straight to the principal. Both strategies will decrease your overall loan costs.

For private loans, making on-time, in-school payments can result in a potentially lower interest rate, said Chris Ebeling, head of student lending at Citizens, a private financial institution. It can also help you build credit, which can be helpful for post-graduate life when you’re looking to rent an apartment or buy a car.

___

States with the highest student loan delinquency rates

States with the highest student loan delinquency rates

Updated

Student loan debt has plagued college graduates for years, with current U.S. debt levels hitting a record-breaking $1.76 trillion. Nationwide, student loan debt decreased since the start of the pandemic, in part due to economic relief efforts such as the CARES Act. While there was a 2.7% increase in 2021 compared to 2020, this represents the lowest year-over-year increase in the last decade—even with the lengthy pause on federal student loan payments due to the COVID-19 pandemic. President Biden announced another extension for federal student loan borrowers until Aug. 31, 2022, to further provide relief.

Student loan debt plays a huge role in restricting financial freedom. Compared to other generations, more millennials have some form of student loan debt. Although they don't have the highest average debt compared to other generations like Gen Xers or baby boomers, about 14.8 million millennials still had some amount of student loan debt to repay, according to Education Data. It’s been one of the reasons why millennials have held off on big purchases such as buying a home; their aversion to debt precludes them from taking out additional loans, including mortgages.

Sound Dollar ranked the states with the highest percentage of student loan delinquencies using 2021 data from FRBNY Consumer Credit Panel/Equifax. States are sorted based on their proportion of student loan borrowers with accounts 90-plus days past due. The dataset also includes the overall total number of student loan borrowers in each state as well as the average student debt balance for each state. Both federal and private student loans are covered in this dataset.

Of all the states mentioned on this list, 10 out of 13 are located in the Southern region of the U.S. Student loan debt is also the second-highest consumer debt category, with mortgages being first. The Federal Reserve dataset lists the average student debt balance among borrowers across the U.S. as $36,200.

![]()

Arkansas

Updated

- Delinquency rate: 9%

- Total number of borrowers: 373,900

- Average student debt balance: $32,400

Kentucky

Updated

- Delinquency rate: 9%

- Total number of borrowers: 586,000

- Average student debt balance: $33,400

Alabama

Updated

- Delinquency rate: 9%

- Total number of borrowers: 614,900

- Average student debt balance: $37,500

Louisiana

Updated

- Delinquency rate: 9%

- Total number of borrowers: 639,300

- Average student debt balance: $35,000

South Carolina

Updated

- Delinquency rate: 9%

- Total number of borrowers: 748,800

- Average student debt balance: $37,200

Tennessee

Updated

- Delinquency rate: 9%

- Total number of borrowers: 867,800

- Average student debt balance: $36,200

Indiana

Updated

- Delinquency rate: 9%

- Total number of borrowers: 926,500

- Average student debt balance: $32,900

Georgia

Updated

- Delinquency rate: 9%

- Total number of borrowers: 1,639,600

- Average student debt balance: $41,600

West Virginia

Updated

- Delinquency rate: 10%

- Total number of borrowers: 215,900

- Average student debt balance: $32,500

New Mexico

Updated

- Delinquency rate: 10%

- Total number of borrowers: 217,700

- Average student debt balance: $34,400

Nevada

Updated

- Delinquency rate: 10%

- Total number of borrowers: 346,200

- Average student debt balance: $35,800

Oklahoma

Updated

- Delinquency rate: 10%

- Total number of borrowers: 474,100

- Average student debt balance: $32,100

Mississippi

Updated

- Delinquency rate: 11%

- Total number of borrowers: 417,600

- Average student debt balance: $37,500

This story originally appeared on Sound Dollar and was produced and distributed in partnership with Stacker Studio.