The tax rate inside the Tucson city limits is 8.6 percent — that's a combination of 5.6 percent for the state of Arizona, 0.5 percent for Pima County and 2.5 percent for the city of Tucson. If you buy one item at one of the $1 stores — it costs $1 — the tax is 8.6 cents ($0.086), but the merchant rounds up, as is legal, and you'll pay 9 cents ($0.09).

If you are fortunate enough to find something somewhere that costs 5 cents ($0.05), first: that's amazing; second: the sales tax is 43/100 of a cent ($0.0043), which is less than ½ of a cent. Chances are, you won't be charged a sales tax because the amount is rounded down.

We might assume that the governments charging that tax are essentially OK with that because you can't really buy anything for a nickel anyway and they got to round up when you bought something for a dollar.

However, back in 1937, there were a lot more things one could buy for a nickel.

People are also reading…

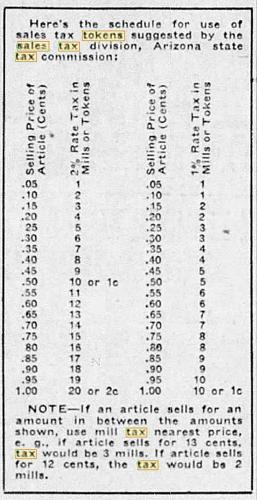

The sales tax in Arizona was 2 percent on most retail items, which means one would pay 2 cents ($0.02) sales tax on an item that costs $1. That would also mean that for items costing less than 25 cents ($0.25) if merchants rounded down, you would not pay a sales tax. This is assuming you only purchased the one item because, of course, the sales tax is calculated on the total purchase.

Fortunately for consumers and unfortunately for the tax commission and local governments, there were quite a few items costing 25 cents or less back then, and Arizona wanted to charge tax on them. Without half-cent coins, and with the law stating only the federal government can make legal tender including coins, the city had to find a way to collect tax on these purchases.

They began minting tax tokens that represented one-tenth and five tenths of a cent. They were called one mill and five mill tokens. The name comes from the fact that a one mill token represents $0.001 or one one-thousandth of a dollar. "Mill" refers to thousand in Latin.

The photo shows (left to right) a quarter, a 5-mill token, a dime and a 1-mill token. One might guess consumers had to pay attention to the coins in their pockets.

This allowed consumers to pay a 1 mill tax on an item that cost 5 cents ($0.05). A consumer would rarely escape a sales tax this way.

Once the tokens were available, there was plenty of confusion. (The Morgue Lady assumes her explanation hasn't confused you already.)

From the Arizona Daily Star, Thursday, Sept. 2, 1937:

How to Use New Tax Tokens

With the new sales tax tokens flowing into the commercial life of the community yesterday in a steady stream, considerable confusion regarding the use of the tokens became evident and tax commission officials were kept busy with explanations.

Ed H. Basye, manager of the Tucson division of the commission, outlines several elements on which the public appeared to be doubtful:

Distribution

1. The plan of distribution is that the general public obtains the tokens through merchants, who obtain their supply at the tax commission office.

Merchants get the tokens at face value, in two denominations; one-mill and five-mill. The merchant will use them in making change on taxable purchases. That is, the tax on a five-cent purchase (either one or two per cent classification), would be one mill. The customer tenders six cents and the merchant gives him nine one-mill tokens, or four one-mill and one five-mill, in change.

Thereafter, the same customer can tender a five-cent piece and a one-mill token for a similar purchase until his supply of tokens is exhausted. When that occurs, he gets more tokens when he offers an excess amount of cash.

Number Needed

2. In determining how many tokens he should buy, the merchant first must analyze his business to see whether purchases made in his store take one or two percent sales tax. Then he must determine in what bracket his average sale falls —10, 15, 35 cents, etc.

He then can arrive at a pretty good guess as to the ratio of one-mill and five-mill tokens he should obtain.

If Tax Absorbed

3. Merchants who don't add the tax to the purchase, but absorb it themselves, need not buy tokens. Basye pointed out, however, that the use of tokens will enable merchants who heretofore have absorbed the tax to add it to the purchase.

Credit Accounts

4. The tax bill of customers maintaining credit accounts will be based on the entire account and not the individual item, with the merchant using his own discretion as to absorption of fractional portions or collection of the fractions in mills.

Who May Obtain

5. Not only merchants, but individuals can obtain the tokens at the tax comission office.

Redemption

6. In turn, the tokens will be redeemed at face value by the tax commission. The merchant cannot pay his tax in tokens, but if he has $10 worth of tokens and owes $10 in tax, he can redeem the tokens for cash and pay the cash on the tax.

This, as well as the statement on the tokens that they are for making changes on taxes, is to bring the tokens inside the constitutional prohibition of manufacture of currency by any political unit other than the federal government.

Tax Classifications

Business classifications covered by the two per cent sales tax include retail, rentals (including hotels and parking lots), and amusements.

Classifications covered by the one per cent tax include transporting, mining, utilities, communications, railroads, pipe lines, publishing, job printing and contracting. The rate is one-quarter of one per cent on manufacturing, meat packing and the wholesale feed business.

Tomorrow, we'll tell you of a problem the tokens caused for slot machine operators.

Johanna Eubank is an online content producer for the Arizona Daily Star and tucson.com. Contact her at jeubank@tucson.com

About Tales from the Morgue: The "morgue," is what those in the newspaper business call the archives. Before digital archives, the morgue was a room full of clippings and other files of old newspapers.

Johanna Eubank

Online producer